Date: May 5, 2025

By JournalFrame News Desk

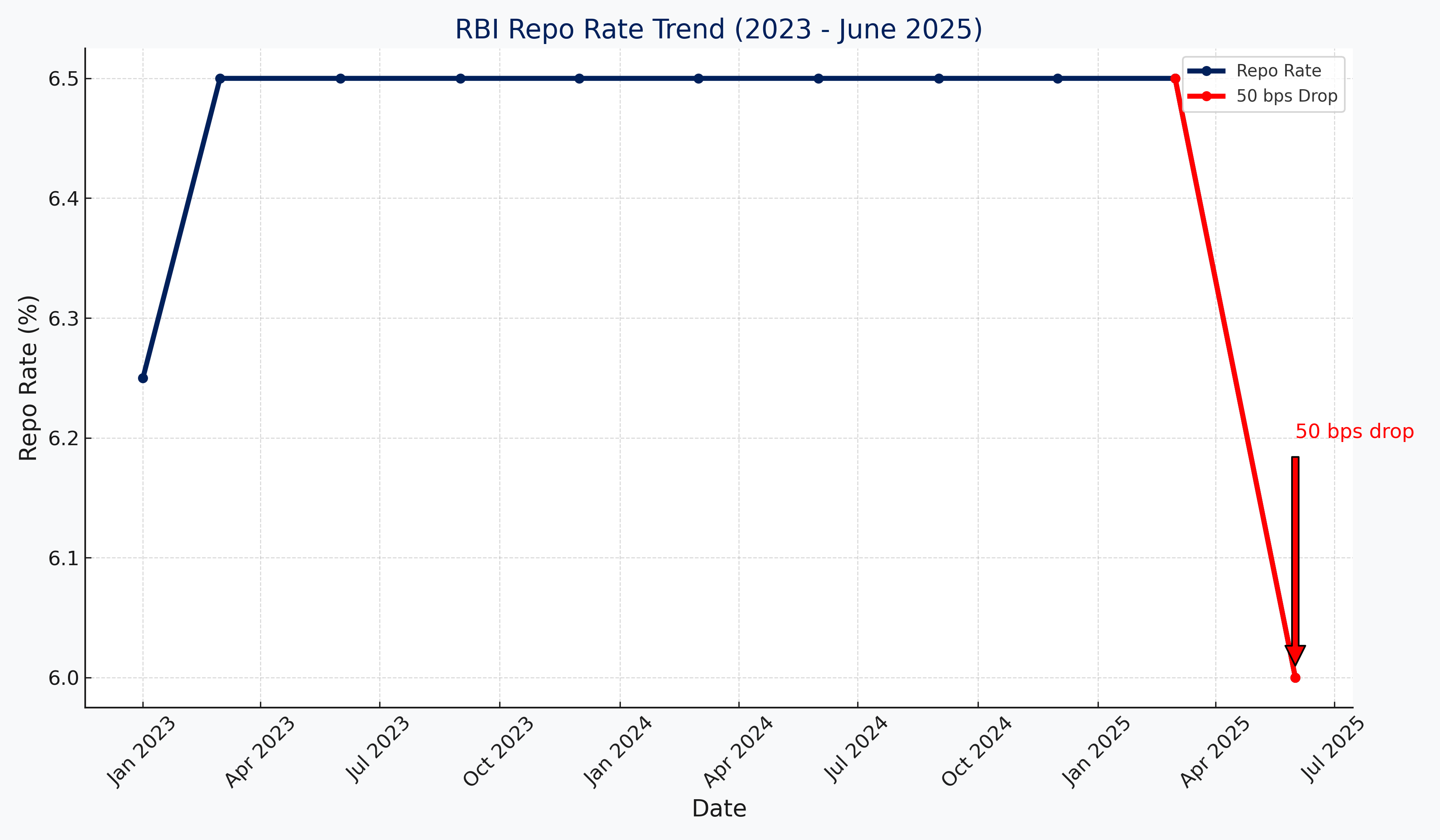

The Reserve Bank of India (RBI) in a 25 basis points rate hike on the repo rate raised it to 6.75% on Monday in its bi-monthly monetary policy meeting. This is the second time for 2025 as the central bank continues battling inflation and holding macroeconomic steadiness.

Repo Rate: What Is It?

The repo rate is the rate at which the RBI lends to commercial banks. If the RBI raises this rate, it becomes costly for banks to borrow—and they, in turn, transfer this expense to consumers.

What It Means for You

1. Home Loans and EMIs to Get Costlier

If you are a floating-rate home buyer, your EMIs will soon go up. All major banks and NBFCs are set to increase interest rates following the rate hike.

Example:

For a ₹30 lakh home loan for 20 years, a 0.25% rise in interest rates can push up the EMI by ₹500–₹700 per month.

Tip: You could possibly increase your EMI marginally to ensure that the loan period is comfortable.

2. Car and Personal Loans Will Also Be Impacted

Banks tend to hike lending rates in general. So if you are considering availing a car loan, personal loan, or consumer durables loan, expect relatively higher interest rates, which will make the overall repayment costlier.

3. Good News for Savers and FD Investors

On the positive front, a repo rate increase tends to prompt banks to increase fixed deposit (FD) rates. That is good news for conservative investors and retirees.

Large banks are likely to hike their FD rates in the next few weeks.

Senior citizens will soon witness FD returns reaching 7.5–8% once again.

4. Why RBI Hiked the Rate Again

RBI Governor Shaktikanta Das mentioned ongoing inflationary pressures, increasing crude oil prices, and geopolitical tensions as grounds for the increase. The central bank is still determined to bring inflation within the 4% target range.

“The MPC believed that calibrated tightening is required to anchor inflation expectations,” said Governor Das.

Market Reaction

The BSE Sensex declined by 250 points immediately after the announcement.

Banking stocks, however, showed resilience due to potential margin improvement from higher lending rates.

Final Thoughts

While the RBI’s decision may feel like a pinch for borrowers, it’s aimed at safeguarding long-term economic stability. As interest rates climb, it’s a good time to:

Compare loan rates before borrowing

Lock in FD rates for medium-term savings

Review your financial plan to manage rising EMIs

Get the latest on Indian economy, finance, and policy from JournalFrame.com.